Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

The First-Time Buyer’s Roadmap in the SF Bay Area: From Saving to Closing

A Step-by-Step Guide to Buying Your First Home in One of America’s Most Competitive Markets

Buying your first home in the San Francisco Bay Area can feel overwhelming. With high home prices, competitive bidding, and constantly changing mortgage rates, many aspiring buyers wonder if homeownership is even possible.

Thousands of first-time buyers successfully purchase homes in the Bay Area every year. Success starts with understanding the process and planning ahead.

Whether you’re dreaming of a condo in San Jose, a townhome in Fremont, or a single-family home in Gilroy or Morgan Hill, this roadmap will help you navigate the journey from saving for a down payment to receiving the keys to your new home.

Step 1: Determine Your Homeownership Goal

Before looking at listings, take time to define what you’re trying to achieve.

Ask yourself:

- Do you want a starter home or a long-term home?

- How long do you plan to stay on the property?

- What commute are you comfortable with?

- Are schools important?

- Would you consider a condo or townhome to enter the market sooner?

Many first-time buyers focus only on price and overlook lifestyle factors. The right home should support both your financial goals and your daily life.

Bay Area Tip:

Expanding your search radius by just 15–20 miles can dramatically improve affordability. Areas like Gilroy, Morgan Hill, Hollister, and parts of Contra Costa County often provide significantly more home for the money than core Silicon Valley locations.

Figure 1: Where affordability meets opportunity in the Bay Area.

Step 2: Build Your Down Payment Strategy

A common myth is that buyers need 20% down. Many loan programs allow much lower down payments.

Common options include:

| Loan Type | Typical Down Payment |

| Conventional | 3%–5% |

| FHA | 3.5% |

| VA | 0% |

| Jumbo Loans | Often 10%–20% |

For a $900,000 home:

- 20% down = $180,000

- 10% down = $90,000

- 5% down = $45,000

The difference can mean buying years sooner.

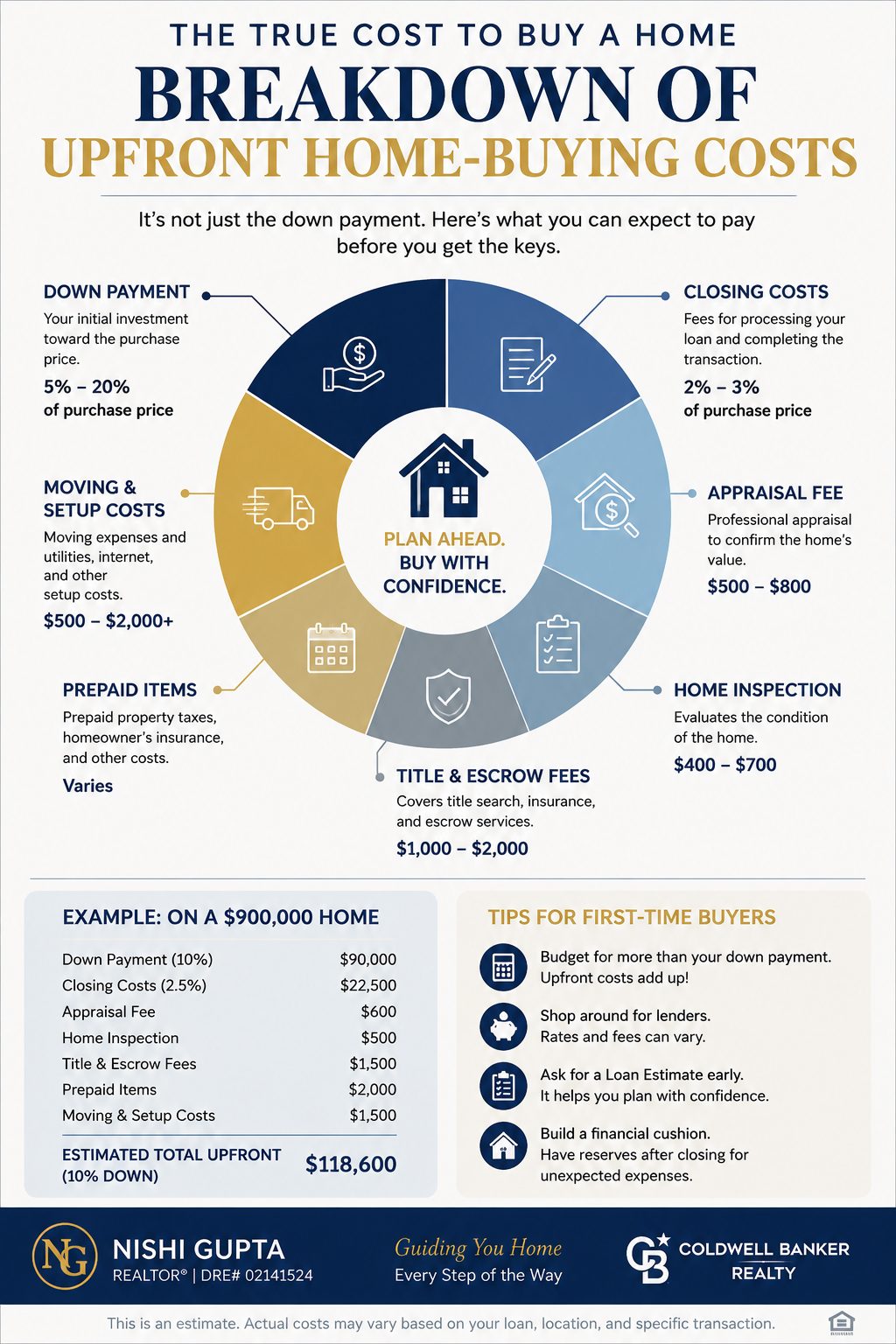

Don’t Forget Other Costs

Besides your down payment, budget for:

- Closing costs (2–3% of purchase price)

- Appraisal fees

- Home inspection costs

- Moving expenses

- Initial repairs or upgrades

Figure 2: It’s not just the down payment—understand the full cost of buying a home.

Step 3: Strengthen Your Financial Position

Mortgage lenders evaluate three primary areas:

Credit Score

Generally:

- 740+ = excellent

- 700–739 = good

- 660–699 = acceptable

- Below 660 may limit options

Debt-to-Income Ratio (DTI)

Most lenders prefer:

- Housing payment below 36–45% of income

- Total monthly debt obligations below lending limits

Cash Reserves

Lenders like to see funds remaining after closing.

Action Items

Before shopping:

✅ Pay down high-interest debt

✅ Avoid opening new credit accounts

✅ Make all payments on time

✅ Continue building savings

Small improvements can significantly impact your purchasing power and interest rate.

Step 4: Get Pre-Approved Before House Hunting

This is where many first-time buyers make a mistake.

They browse homes first and talk to a lender later.

Instead, get pre-approved before attending open houses.

A pre-approval helps you:

- Understand your true budget

- Estimate monthly payments

- Strengthen your offer

- Identify financing issues early

In competitive Bay Area markets, sellers often expect buyers to already have financing lined up.

Bay Area Tip

Work with a lender experienced in local markets. They understand jumbo financing, high-cost county limits, and competitive offer situations.

Step 5: Build the Right Team

Buying a home is easier when you have the right professionals guiding you through the process. For most first-time buyers, the two key members of your team are your Realtor® and lender.

Realtor®

A local Realtor® helps you:

- Market analysis

- Property tours

- Offer strategy

- Negotiations

- Inspections and contingencies

- Closing coordination

Lender

Provides financing guidance and loan approval.

A strong Realtor® and lender team can help make your home-buying journey smoother and less stressful.

Step 6: Start Touring Homes Strategically

Now comes the fun part.

However, successful buyers don’t simply tour random homes.

Create a framework:

Must-Haves

Examples:

- Minimum bedrooms

- School district

- Commute distance

- Garage

Nice-to-Haves

Examples:

- Large yard

- Updated kitchen

- Pool

- Corner lot

Understanding your priorities helps prevent emotional decision-making.

Bay Area Reality

Your first home may not be your forever home. Many successful homeowners start with a condo, townhome, or smaller single-family home and build equity over time.

Step 7: Understand the Offer Process

Once you find the right property, it’s time to submit an offer.

Your offer includes more than just price.

Important terms may include:

- Down payment amount

- Loan type

- Closing timeline

- Inspection contingency

- Appraisal contingency

- Financing contingency

Competitive Markets

In parts of the Bay Area, multiple-offer situations still occur.

Winning often requires:

- Strong financing

- Strategic pricing

- Clean contract terms

- Professional presentation

The highest offer doesn’t always win.

The strongest overall offer often does.

Step 8: Complete Inspections and Due Diligence

After your offer is accepted, you’ll enter escrow.

This is your opportunity to fully investigate the property.

Common inspections include:

- General home inspection

- Roof inspection

- Pest inspection

- Sewer lateral inspection

- Foundation evaluation (if needed)

Review all disclosures carefully.

The goal is to understand the home’s condition and avoid surprises after closing.

Questions to Ask

- Are there safety concerns?

- Are major systems nearing replacement?

- Are there permit issues?

- Are future repair costs likely?

Knowledge creates negotiating power.

Step 9: Final Loan Approval

During escrow, your lender completes the underwriting process.

Avoid major financial changes during this period.

Do NOT:

❌ Buy a new car

❌ Open new credit cards

❌ Change jobs without consulting your lender

❌ Make large unexplained deposits

Even well-qualified buyers can encounter delays if their financial profile changes before closing.

Step 10: Closing Day and Getting the Keys

The final stage includes:

Final Walk-Through

Confirm:

- Agreed repairs are complete

- Home condition remains unchanged

- Appliances and fixtures are present

Sign Closing Documents

Most buyers sign:

- Loan documents

- Title paperwork

- Escrow instructions

Fund the Transaction

Wire remaining down payment and closing funds.

Record and Celebrate

Once the county records the transaction, ownership officially transfers to you.

Congratulations—you are now a homeowner.

Common First-Time Buyer Mistakes to Avoid

Waiting for the “Perfect” Interest Rate

Many buyers delay for years hoping rates will drop.

Meanwhile:

- Home prices may rise

- Inventory may shrink

- Rent continues accumulating

Shopping Beyond Budget

Falling in love with homes outside your budget creates frustration.

Focus on what you can comfortably afford.

Skipping Professional Advice

The Bay Area market is complex.

Experienced local guidance can help avoid costly mistakes.

Underestimating Ongoing Costs

Remember to budget for:

- Property taxes

- Insurance

- Maintenance

- HOA fees (if applicable)

Figure 3: Your roadmap from saving to homeownership.

Final Thoughts

Buying your first home in the Bay Area is a significant milestone. While the process may seem intimidating, breaking it into manageable steps makes it far more achievable.

The buyers who succeed aren’t necessarily those with the highest incomes—they’re often the ones who prepare early, understand the process, and make informed decisions.

Whether you’re six months away from buying or actively searching today, having a roadmap can help turn homeownership from a distant goal into a realistic plan.

The journey may start with saving, but it ends with a place to call home.

Ready to Start Your Homeownership Journey?

Whether you’re just beginning to save for a down payment or actively looking for homes in the Bay Area, I’d be happy to help you understand your options and create a plan that fits your goals.

Nishi Gupta, Realtor®

Coldwell Banker Realty

📞 510-320-9444

🌐 NishiGuptaHomes.com

DRE#02141524